Do Banks Finance Barndominiums?

Yes, **banks do finance barndominiums**, but the process can be a bit more complex than securing a loan for a traditional home. Barndominiums, which combine residential living spaces with functional areas like workshops or storage, are often seen as non-traditional structures, which may cause some banks to approach financing with caution. However, as barndominiums become more popular, more lenders are becoming familiar with them and willing to finance their construction.

In this article, we’ll explain where your best chances of getting barndominium financing might be and explore the best barndominium financing options available in **2024**.

Why Financing a Barndominium Can Be Challenging

Financing a barndominium can be slightly more challenging than financing a traditional home for a few reasons:

1. **Non-Traditional Structure**: Barndominiums are often viewed as non-standard homes, especially if they include large, open spaces like barns or workshops. Some lenders may not understand how to assess their value, which can make securing financing more difficult.

2. **Appraisal Difficulties**: Since barndominiums are less common than traditional homes, finding comparable properties for appraisals can be tricky. Lenders typically rely on appraisals to determine the value of a property, and if there aren’t enough similar properties in the area, it can complicate the approval process.

3. **Construction Loans vs. Mortgages**: If you’re building a new barndominium, you’ll likely need to secure a **construction loan** first, which will convert into a **traditional mortgage** once the home is completed. Some lenders may not offer construction loans for non-traditional homes, so finding a lender with experience in financing barndominiums is important.

Where to Get Financing for a Barndominium

The good news is that several banks and lenders do offer financing for barndominiums, and your chances of getting financing are higher if you work with lenders familiar with these types of structures. Here are some of the best places to secure barndominium financing:

1. **Local and Regional Banks**

**Local and regional banks** often have more flexibility in lending and may be more willing to finance barndominiums. These smaller banks are often more familiar with the local market and may have more experience financing non-traditional homes in rural areas where barndominiums are more common.

– **Advantages**: Local banks may have more lenient lending policies for unique properties like barndominiums, especially in rural or agricultural areas where they are more popular.

– **Best Chance**: If you live in a region where barndominiums are common (such as Texas, Oklahoma, or the Midwest), local banks are often the best starting point for financing.

2. **Credit Unions**

**Credit unions** are another excellent option for barndominium financing, as they often provide more personalized service and may be willing to work with borrowers to secure non-traditional financing. Credit unions tend to be more community-focused and may be more flexible in approving loans for unique properties.

– **Advantages**: Credit unions often offer **lower interest rates** and more flexible terms than large national banks. If you already have an account with a credit union, you may have an easier time securing a loan for your barndominium.

3. **Specialized Lenders for Construction Loans**

If you’re building a new barndominium, you’ll need a **construction loan** to finance the build. Construction loans are short-term loans that provide the necessary funds to construct your home, and once the construction is complete, the loan is converted into a traditional mortgage.

Some lenders specialize in **construction-to-permanent loans** that can finance both the construction and long-term mortgage for your barndominium. These lenders are more familiar with unique or custom builds like barndominiums.

– **Advantages**: Construction-to-permanent loans combine both the construction and mortgage process into one, simplifying financing. Specialized lenders may also be more familiar with the challenges of building a barndominium, making the approval process smoother.

Best Barndominium Financing Options in 2024

In **2024**, several financing options are available for building or buying a barndominium. Here are some of the best options to consider:

1. **FHA Loans**

The **Federal Housing Administration (FHA)** offers loans with low down payment requirements (as low as 3.5%) and flexible credit score requirements. FHA loans are a popular choice for first-time homebuyers, and while they are typically used for traditional homes, some lenders may offer FHA loans for barndominiums if they meet certain requirements, such as being used primarily as a residential space.

– **Advantages**: Low down payment and flexible credit requirements.

– **Challenges**: FHA loans can only be used for properties that meet **primary residence** guidelines, so if a significant portion of your barndominium is used for non-residential purposes (like a workshop or barn), it may not qualify.

2. **USDA Loans**

**USDA loans** are offered by the **U.S. Department of Agriculture** and are designed to help people build or buy homes in **rural areas**. Barndominiums are often built in rural areas, making them a great candidate for USDA loans. These loans come with no down payment requirement and offer competitive interest rates.

– **Advantages**: No down payment required, and competitive interest rates for rural properties.

– **Challenges**: Your barndominium must be located in an eligible rural area, and the property must meet USDA guidelines for residential use.

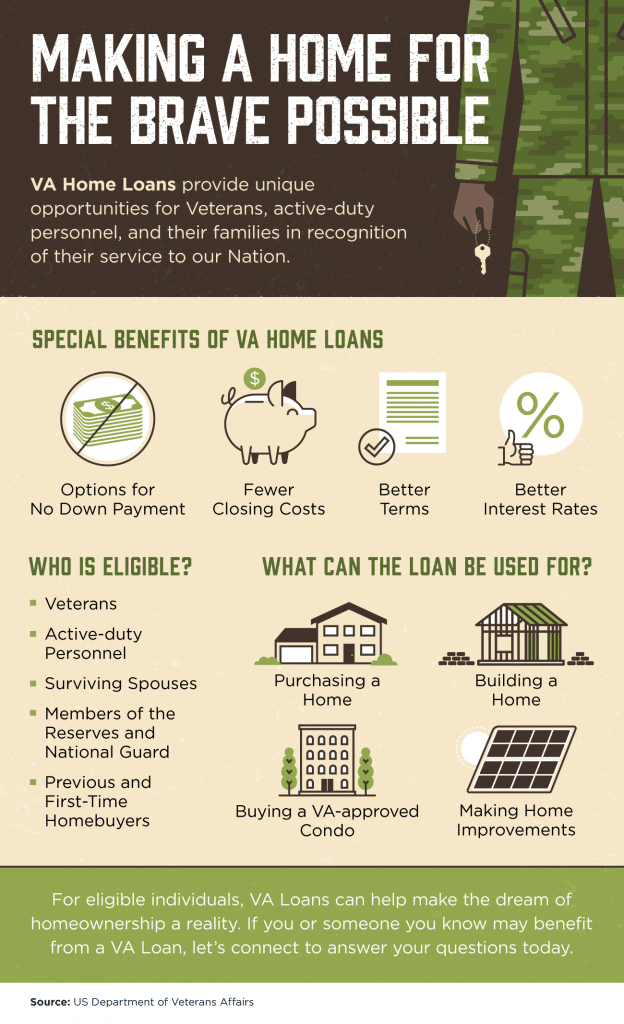

3. **VA Loans**

If you’re a veteran or an active-duty member of the military, you may be eligible for a **VA loan**. VA loans offer **zero down payment** and **no private mortgage insurance (PMI)**, making them an attractive option for financing a barndominium. While VA loans are typically used for traditional homes, some lenders will approve them for barndominiums as long as the property is primarily a residence.

– **Advantages**: No down payment, no PMI, and low-interest rates for eligible veterans and active-duty service members.

– **Challenges**: Like FHA loans, VA loans are only available for homes that serve as primary residences. Non-residential portions of your barndominium may complicate approval.

4. **Conventional Loans**

**Conventional loans** are another popular option for financing barndominiums, especially if the property is primarily residential. Many lenders offer conventional loans, and as barndominiums become more mainstream, conventional loans are becoming easier to secure for these types of homes.

– **Advantages**: Conventional loans typically offer competitive interest rates, and many lenders are willing to approve loans for barndominiums.

– **Challenges**: You may need a higher down payment (often 10% to 20%) and good credit to qualify for a conventional loan.

5. **Construction-to-Permanent Loans**

If you’re building a new barndominium, a **construction-to-permanent loan** is one of the best options. These loans finance the construction of the barndominium and then convert into a traditional mortgage once the construction is complete. This type of loan streamlines the financing process by combining construction and mortgage financing into one loan.

– **Advantages**: Simplifies the financing process and reduces the need for multiple loans. Many lenders offer these loans specifically for custom homes and barndominiums.

– **Challenges**: You’ll need to work with a lender who understands barndominium construction to ensure the loan covers both the build and the long-term mortgage.

Conclusion: Barndominium Financing Is Available with the Right Lender

While securing financing for a **barndominium** may be slightly more challenging than for a traditional home, it’s certainly possible with the right lender. Your best chance of securing financing is through **local banks**, **credit unions**, or lenders who specialize in **construction loans**. Additionally, **FHA**, **USDA**, **VA**, and **conventional loans** are viable options if your barndominium meets the required guidelines for residential use.

As barndominiums continue to grow in popularity, more lenders are becoming familiar with these unique structures, making financing more accessible in **2024**. By working with the right lender and exploring different loan options, you can secure financing and move forward with building or buying your dream barndominium.