Despite the growing popularity of barndominiums for their cost-effectiveness, versatility, and stylish design, securing financing for them can present challenges. It can be down Right Difficult to be perfectly blunt. This attitude towards Barndominiums stem from several factors related to the banking and financing industries’ preconceived perceptions and policies regarding non-traditional residential properties. Here’s a detailed look into why banks might be hesitant to finance barndominiums and the intricacies of bank loan approval in this context.

Appraisal and Valuation Issues

One of the most significant hurdles in securing financing for a barndominium is the challenge of obtaining an accurate appraisal. Banks require appraisals to determine the property’s value, which in turn, informs their lending decisions. Because barndominiums are relatively unique and fewer in number compared to traditional homes, finding comparable sales (comps) necessary for accurate valuation is difficult. Without reliable comps, banks face uncertainty in assessing the true market value of a barndominium, making them less inclined to offer financing.

Marketability and Resale Value

Banks consider the resale value and marketability of a property when approving loans. Traditional homes, with their widespread appeal and demand, are seen as less risky investments. Barndominiums, on the other hand, cater to a niche market. Their unique style and the fact that they’re often located in rural or semi-rural areas can limit potential buyers. This perceived risk of difficulty in selling the property, should the need arise, makes banks wary of offering loans for barndominiums.

Zoning and Regulatory Challenges

Another complicating factor for financing barndominiums is the zoning and regulatory environment. Barndominiums can sometimes fall into a gray area between residential and agricultural or commercial zoning regulations. This ambiguity can pose challenges for banks, as the potential for zoning disputes or non-compliance with local regulations adds a layer of risk. Furthermore, some municipalities may have stringent requirements or lack clear guidelines for barndominiums, complicating the approval and construction process.

Construction and Durability Perceptions

Despite many barndominiums being constructed with high-quality materials and modern techniques, there’s a perception among some lenders that these structures may not be as durable or long-lasting as traditional homes. Concerns about the structural integrity of a metal building, potential for damage from environmental factors, and overall longevity can influence a bank’s decision. Additionally, because barndominiums often involve a combination of residential and workshop or agricultural spaces, there may be concerns about wear and tear or the use of materials not typically found in residential construction.

Financing Product Availability

The financial products available for purchasing or constructing traditional homes are well-established, with clear guidelines and a long history of performance data. In contrast, barndominiums may not fit neatly into the categories defined by conventional mortgage products. This lack of a standardized financing pathway means banks may have to venture into uncharted territory to lend for a barndominium project, something many are reluctant to do without clear guidelines and precedents.

Interest Rates and Loan Terms

When financing for barndominiums is available, it often comes with less favorable terms than those for traditional homes. Higher interest rates and down payment requirements reflect the bank’s perception of higher risk. These conditions can make securing financing more costly for the borrower, potentially offsetting some of the cost savings that make barndominiums attractive in the first place.

When financing a barndominium in 2024, you have several loan options available, each with its own set of terms, interest rates, and eligibility requirements. Here’s a summary of the main financing options:

1. **Conventional Loans**:

– Offered by banks, credit unions, and national lenders.

– Require a down payment (usually between 3% and 20%) and have terms usually between 15 and 30 years.

– The exact terms and interest rates vary by lender.

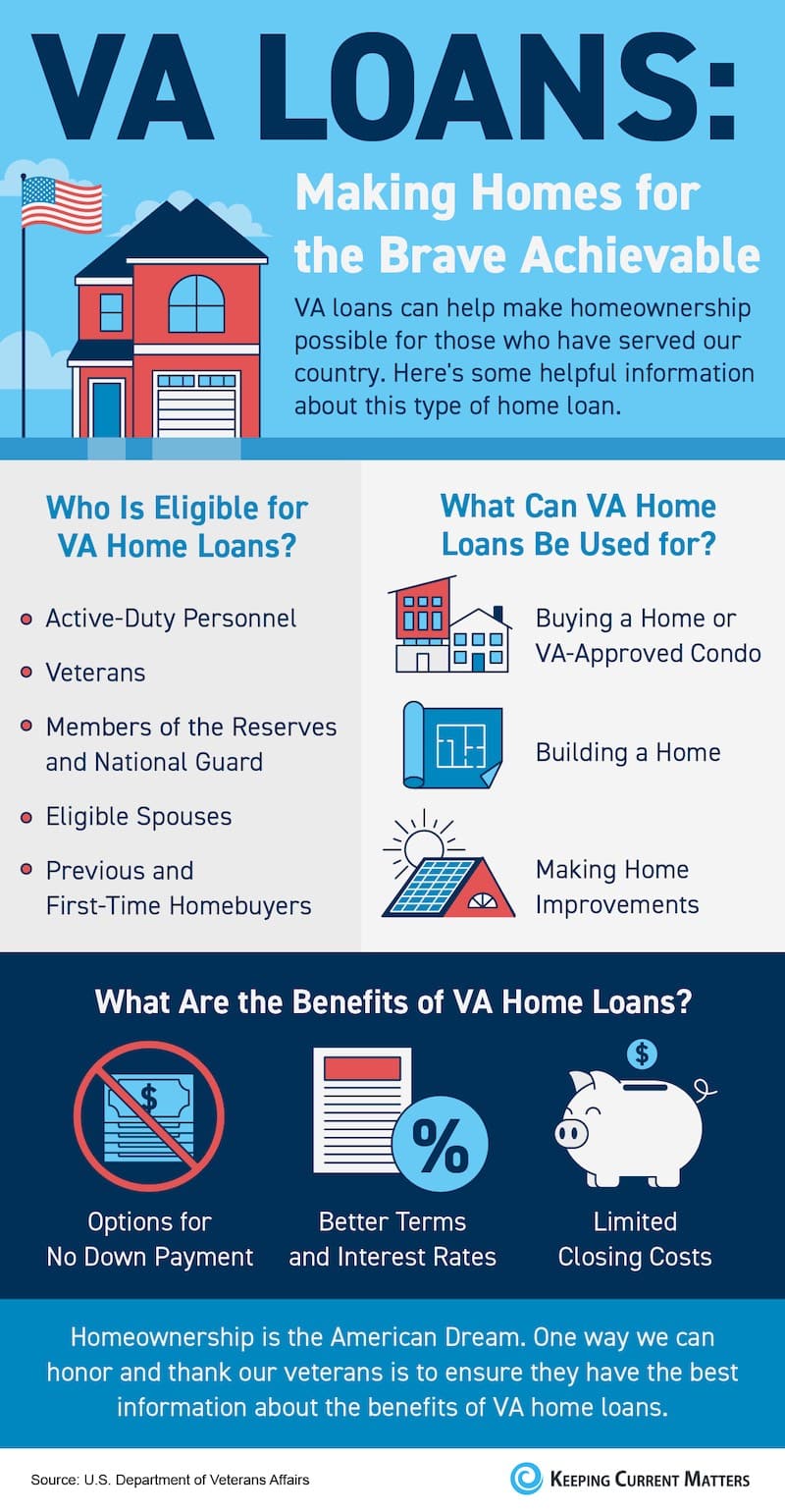

2. **VA Loans** (for veterans or active military members):

– Require no down payment and no mortgage insurance.

– Offer lower interest rates compared to conventional loans.

– Have specific eligibility criteria, but no minimum credit score requirement.

– Feature limits on lender charges for closing costs to 1% of the loan【6†source】.

– The VA guarantees these loans, making them less risky for lenders【9†source】.

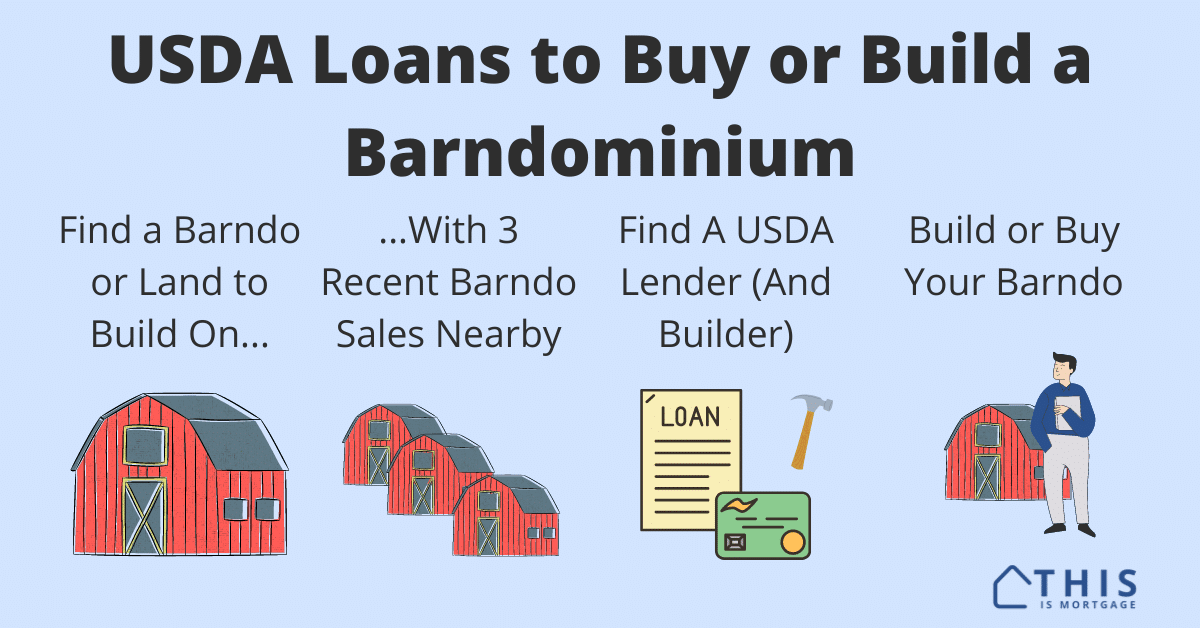

3. **USDA Loans** (for rural areas):

– Require no down payment.

– Include an upfront fee (typically 1% of the total loan amount) and an annual fee (usually 0.35% of the remaining principal balance), which are generally lower than FHA and conventional mortgage insurance premiums【7†source】.

– Offer the possibility to finance both land and construction costs【7†source】.

– Eligibility depends on the location and household income, with specific debt-to-income ratio limits【7†source】.

4. **FHA Loans**:

– Can cover land, permits, construction, and building materials.

– Require small down payments of just 3.5%.

– Have stringent requirements for qualifying【8†source】.

When considering financing for a barndominium, it’s crucial to understand the various types of loans available and their respective requirements and benefits. For instance, conventional loans often necessitate a substantial down payment and good credit, while USDA and VA loans offer no down payment options, which can be particularly beneficial for certain buyers.

Additionally, when applying for a loan, lenders will evaluate your credit worthiness, the property’s location, and detailed plans for the construction, including fixtures, amenities, and finishes. It’s important to be prepared with all necessary documentation and a clear understanding of your budget and financing needs【5†source】.

Interest rates and loan terms can vary widely based on the type of loan, the lender, and the borrower’s credit profile, among other factors. Therefore, it’s advisable to research thoroughly and compare different loan options and lenders to find the best fit for your financial situation and housing needs.

Navigating the Challenges

For prospective barndominium owners, understanding these challenges is the first step in navigating them. Working with lenders who have experience in non-traditional properties or seeking out specialized financial institutions that offer products tailored for barndominiums can be beneficial. Additionally, preparing a detailed appraisal report, including comps of similar properties if available, and presenting a clear, compliant plan addressing zoning and regulatory requirements can help mitigate some of the concerns lenders may have.

In conclusion, while financing a barndominium can be more complex than securing a mortgage for a traditional home, it’s not impossible. Awareness of the issues and proactive engagement with potential lenders can pave the way for financing these unique and increasingly popular homes.